At the end of the year, you often read that you should quickly set up a holding company in order to benefit from a tax-free profit distribution from the holding companies next year. But that’s not true across the board!

What exactly is it about?

If a corporation (such as a GmbH) distributes profits to another corporation, these are generally subject to corporation and trade tax. This applies regardless of whether the corporation is engaged in commercial or asset management activities. This is because a corporation is subject to trade tax even if it does not engage in any commercial activity.

But: Profit distributions (from 10 % for corporation tax purposes (Section 8b (4) KStG)and from 15 % for trade tax (§ 9 No. 2a GewStG)) are 95% tax-free – this means that at the level of a corporation only a minimal tax burden of around 1.5% on the on the profit distribution is incurred.

However, the prerequisite for preferential tax treatment for trade tax purposes is that the amount of the shareholding is already known at the beginning of the calendar year or of the assessment period (Section 14 GewStG).

Pitfall with a "spontaneous" holding company formation

If a holding corporation is founded in the middle of the year, the shares of another corporation are transferred to it and a profit distribution is made in the same year, there is a risk that the trade tax requirements of section 9 no. 2a GewStG are not met. In this case, the profit distribution would be fully subject to trade tax. It is important to note that the decision to distribute profits is already decisive for tax purposes. Profitdistribution – not just the time of payment.

For corporation tax purposes, Section 8b (4) sentence 6 KStG stipulates that the acquisition of an equity interest of at least 10% during the year is treated as if the interest already existed at the beginning of the year, which means that the conditions for extensive tax exemption are usually met. However, this regulation does not apply to trade tax!

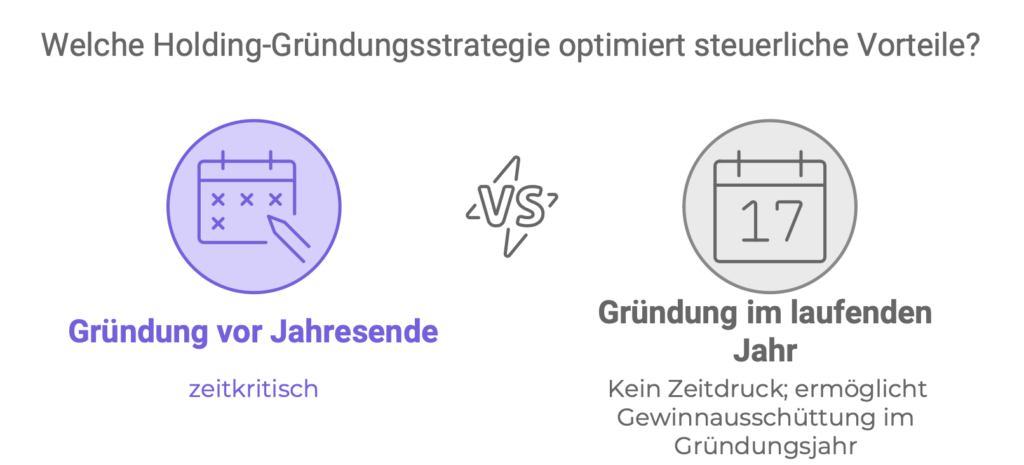

How do you optimize taxes?

There are two approaches to setting up a tax-optimized holding company:

In the first variant, the time pressure can be problematic in order to complete the formation in time before the end of the year.

In the second variant, however, the time factor does not play a role, as a tax-privileged profit distribution is already possible in the year of formation. In this case, the shares are transferred directly to the holding company when it is founded. At this point, there is generally no trade tax liability, which only begins when the holding company is entered in the commercial register.

The decisive factor for trade tax exemption in the case of profit distributions in newly established companies is the level of shareholding at the time the trade tax liability begins. This requirement would be met if the holding corporation held at least 15% of the shares at this time.

The BFH has confirmed this structure (see BFH ruling of 24.01.2017 – I R 81/15, BStBl. II 2017 p. 1071), and the tax authorities are following this case law. With correct planning, a tax-privileged profit distribution can therefore already be made in the year of formation.

Do you have any questions on this topic?

Conclusion and important note

Setting up a holding company can be worthwhile from a tax perspective, but the timing and structure are crucial. Please note that the transfer of shares to a holding company may trigger taxation of hidden reserves if there is no option for a tax-neutral restructuring.

If you have any questions or need support, we are always at your disposal.

The author: Timo Unterberg

Anyone who knows me knows that tax law is my passion! When I am not advising young growth companies and medium-sized corporate clients on restructuring, financing issues or corporate succession, I am on the road as a lecturer in tax consultant training and continuing education. I also regularly write tax-related articles for specialist journals.